Corona boosts rethinking in the German automotive industry

Will the Corona pandemic save the German automotive industry? The Corona crisis is currently changing our view of mobility. On the one hand for ourselves as the basis of our personal autonomy and on the other hand for our economy as the basis for prosperity. Germany now has the opportunity – fueled by the COVID19 pandemic – to benefit from the imminent mobility revolution and emerge stronger.

Mobility as a basic need AND fundamental right

What will change with and after Corona? The more our mobility is restricted, the more we become aware of it. Unthinkable until recently: (behavioural) rules, whether, how and where we are allowed to move. We are more considerate of each other and restrict ourselves. We get creative and change our motion culture: bike instead of car and bus, hiking instead of cable car, home office instead of commuting 45 minutes a day to the workplace. Our attitudes and behaviour are changing. On the one hand, our proven crisis manager Angela Merkel apologizes for these restrictions on our fundamental right. On the other hand, our car chancellor promises extensive support to the car industry to respond to the fear of job loss. The demanded purchase incentives for high-powered fossil vehicles from the excess of German car manufacturers do not lead out from a dead-end, but to a fatal ghost ride in the wrong direction.

Direction and speed are now dictated by others

With climate protection, alternative drive technologies, digitalization and changing mobility behaviour, the industry is facing its biggest challenge. „The automotive industry will change more in the next 5 years than in the last 100 years.“ said the German automotive CEOs unanimously for the 100th birthday of the automobile in 2016. The direction and the speed were and are given by others, especially Tesla. Soon also in automotive stronghold Germany with its own factory.

Future mobility: The how and not the what is in the forefront

Global developments determine the pace of the current reinvention and transformation of the automotive industry: Possible penalties due to emission regulations force decarbonisation and thus the electrification of vehicle fleets. In the long term, combustion engines (diesel/gasoline and gas) will be replaced by electric motors (battery and fuel cell). As a bridge technology, hybrid engines will continue to gain in importance in the next decade. In addition to drivetrains, the mobility revolution is driven primarily by the opportunities offered by digitalization. The HOW and not the WHAT is in the forefront in the future, when we move or are moved from A to B.

Proud of our car industry is crumbling

Now is the time to act boldly and make swift decisions. Companies in the automotive industry must now set the course for successfully coping with the inevitable change. If our German automotive industry does not ad0pt to the future or adopt too late, they risk of loss of value creation. A significant proportion of the estimated 1.8 million jobs currently depend on the combustion engine. COVID-19 acts as a fire accelerator for the transformation to electric drivetrains. This is accompanied by the insecurity of employees and customers as well as the crumbling identification and pride in our automotive industry. Our future mobility is controversially discussed in families, in (social) media and in debates.

Odyssey in the wrong direction

Even before the Corona pandemic, the car industry was under enormous pressure. As the formerly richest municipalities in Germany, Wolfsburg and Ingolstadt begged the Chancellor for support with the argument of safeguarding existing jobs. Their research and development has invested too little in future-proof sustainable drivetrains, but above all in larger/heavier and more luxurious products. Especially in the highly demanded SUVs, which follow our desire for safety, driving pleasure and convenience. The amount of resources needed to get us from A to B has increased significantly over the last 25 years. Between the VW Golf of 1995 and the current VW Golf, its area has increased by 12% and its weight by 25%. The average PS number of new passenger cars has grown by 66% during the same period. Do we now need the promotion of micro-mobility as a counter-movement?

Conflict between economic and ecological footprint

As a result of the Corona pandemic, critical economic decisions are urgently needed. This crisis has dramatically increased the speed and pressure to manage this change. This crisis offers the opportunity to make our mobility more sustainable and intelligent. It is now important to keep an eye on climate targets and the economy equally. The automobile industry must not make the mistake of missing this opportunity to change on the way to rehabilitation.

In addition to the ecological decisions that have been discussed for years, the next step – as a result of the Corona pandemic – is to make trendsetting economic decisions. COVID-19 has dramatically increased the speed and pressure to manage this change. This is not about the question: „Ecology OR Economics?“ but rather the sustainable and more intelligent design of our mobility in the direction of „Ecology AND Economy!“ In order to ensure the preservation and safeguarding of jobs and the achievement of our climate targets in the mobility sector, it is important to support the automotive industry in its transformation in a targeted manner when restarting.

EXCURS with a glimpse to Austria as an orientation

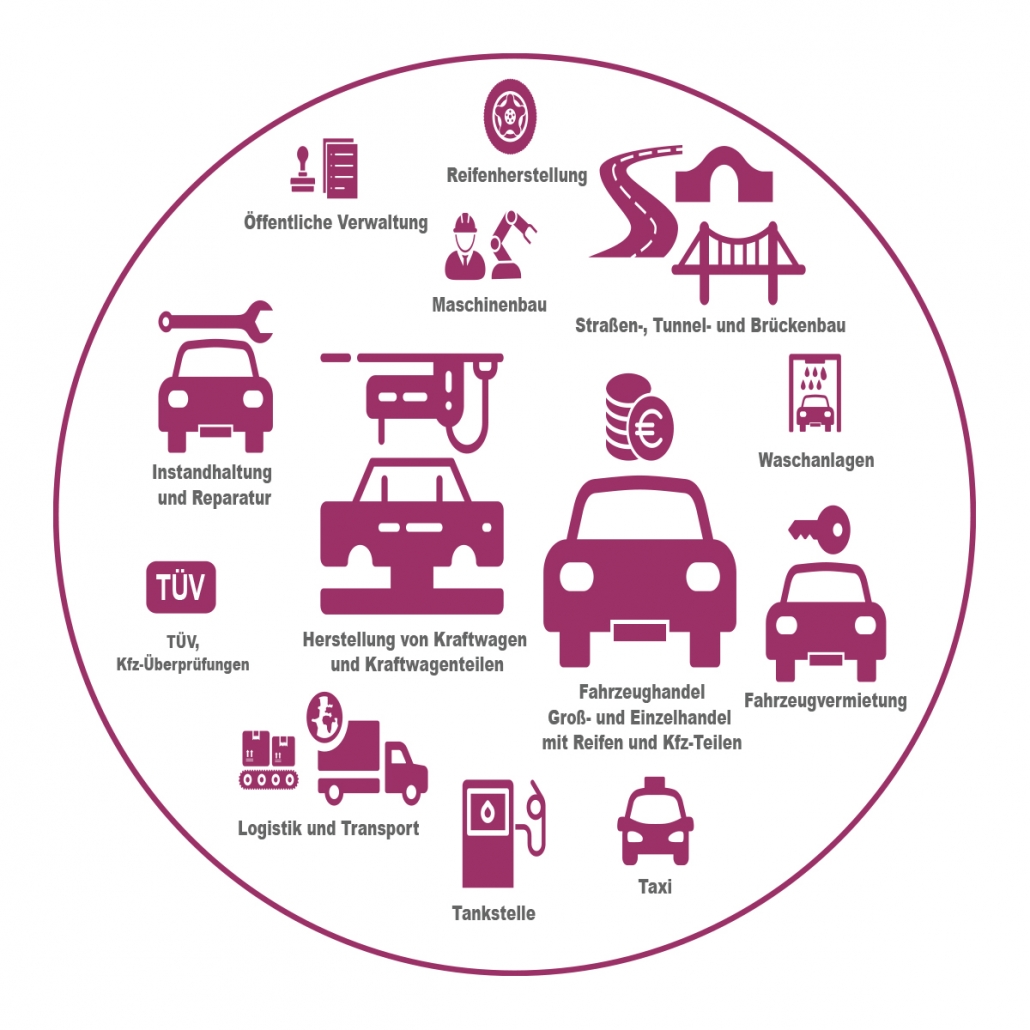

The German automotive industry is undoubtedly the key sector of the German economy. The automotive industry is closely intertwined with a variety of sectors, thus securing jobs not only directly, but also indirectly. However, there are only estimates of how many jobs in Germany depend on car production.

An indicative view to our neighbour Austria can help here. The Austrian Federal Ministry for Climate Protection, Environment, Energy, Mobility, Innovation and Technology (BMK) and the Federation of Austrian Industries (IV) have joined forces to commission a study on the transformation of the automotive industry. Building on the economic importance of the automotive industry (which, in addition to production, also includes trade, repair and all other industries related to the automobile, such as car rental, insurance and driving schools), this study primarily examined the effects of drivetrain electrification on the Austrian automotive industry. The aim of the study was to identify opportunities and measures to remain successful as a trusted supplier location for the automotive industry.

Key facts on the Austrian automotive economy:

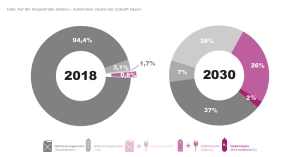

Reference vehicles were determined for each drive technology (combustion engines with diesel, gasoline, gas and hybrids as well as electric vehicles with batteries and fuel cells). For each reference vehicle, it was determined which vehicle components are required, whether they are produced domestically or imported and how their cost structure is defined. It makes a significant difference how the market development of the individual drivetrain technologies will continue in the coming years, as components of electric vehicles (e. g. battery cells) have to be imported more frequently and the value creation is shifting abroad.

Therefore, depending on the speed of electrification, a total of four scenarios were developed.

In the most realistic of these four scenarios, more than one in four cars will be powered by battery (26%) or fuel cell/H2 (2%) by 2030. Hybrid systems will have established themselves as a transitional solution. Internal combustion engines will remain the largest group with 72% over the next 10 years.

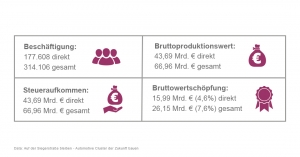

The impact of the different drivetrain technologies on the national economy is not just a matter of looking at the automotive industry. The upstream value chain with suppliers and the downstream, so-called induced and income effects must also be taken into account here. Methodologically, this requires a so-called satellite account for the automotive industry, which maps the entire value-added network within the framework of national accounts.

It forms the basis of the input-output analysis, which enables the calculation of the most important economic indicators such as gross output value, gross value added and employment.

Regardless of whether electrification is slow or rapid, there are positive effects on the development of the gross production value as the value of all goods and services produced domestically. This is mainly due to the significantly higher production costs of electric and hybrid drivetrains compared to internal combustion engines.

However, a look at gross value added, which is more meaningful in terms of economic power, since the required intermediate consumption is deducted from the gross production value, obscures this picture: many of the newly required components are often not produced in Austria, but have to be imported. In the most realistic scenario, value creation in the automotive industry is reduced by 1.7 percent, and in the most ambitious scenario by 5.8 percent, which corresponds to around two billion euros.

A similar picture emerges for the labour market: based on just under 397,000 direct and indirect employees in the automotive economy, 6,000 jobs would already be lost in the real scenario, which corresponds to a minus of 1.5%. In the scenario of extreme electrification, up to 6.1% of jobs would be lost, which corresponds to 25,000 employees.

Core result: Austria is not yet prepared for rapid change. Many companies still depend on the combustion engine for their product portfolio. A massive awareness campaign is needed for customers, companies and retailers. Openness to technology, innovative strength and the appropriate qualifications of employees are fundamental. In addition, politicians and local authorities must work together with industry to create stable framework conditions and manage the transformation professionally.

Fig. Economic Footprint of the Automotive Industry

Accelerate the start of reinvention

Dieselgate and Tesla have highlighted the overdue structural change in the industry. The German car manufacturers – above all VW – have begun the realignment. COVID-19 has now created an existential emergency that needs courage and prospects for a better future. With targeted support for more sustainable energy production, more environmentally friendly drivetrain technologies, the connection of our transport and new mobility services. Governmental funding can help to accelerate the already due change to more sustainability and realign the business foundation for the future.

Master Plan Mobility Transformation

A cross-sectoral „Mobility Transformation Master Plan“ is needed. This can only succeed hand in hand with the energy turnaround and with technology openness. We need an economically and ecologically sustainable industrial policy – based on the Paris climate targets and the modernisation of our industry.

The German automotive industry has the best chances for the future if it becomes even more innovative and sustainable. Because one thing is clear: Their economic footprint will change. The automotive stronghold Germany is transforming itself into a country of mobility.

- Industrial funding instead of consumer promotion. If state aid packages without sustainability orientation are distributed with the watering can, the outdated structures are craved in stone for many years. Every euro of state aid for combustion technology and for the short-term dismantling of vehicles in stockpiles is throwing our automotive industry further back.

- The transition in mobility needs an energy turnaround. The central demand of electromobility must be: Only with sustainable primary energy source electromobility can unfold its full potential.

- Securing Germany as an automotive/mobility stronghold and promoting start-ups: innovation and research must be supported, incentives for investment and innovation must be created with the premise of technology openness.

- New jobs with new skills. New competencies need to be built up, existing engineers, developers and specialists need to be retrained. Without experts for the new drivetrain technologies, connectivity, automation and digital platforms for customers, this technology change and reorientation cannot be mastered.

- Information and education. Our population, entrepreneurs, employees and customers must be enlightened and supported in an opportunity-oriented and fact-based manner by credible and independent experts with in-depth knowledge and in-depth experience.

Germany has the opportunity – fueled by the COVID 19 pandemic – to become a beacon and pioneer of the necessary global mobility revolution and to emerge stronger as an automotive innovator.